A fresh wave of political debate has taken over Nigerian social media following recent comments by Peter Obi, where he questioned the rising debt profile under the administration of Bola Ahmed Tinubu. The statement, now widely shared across platforms like Facebook, Instagram, and X, has sparked intense reactions, with many Nigerians asking tough questions about the country’s economic direction.

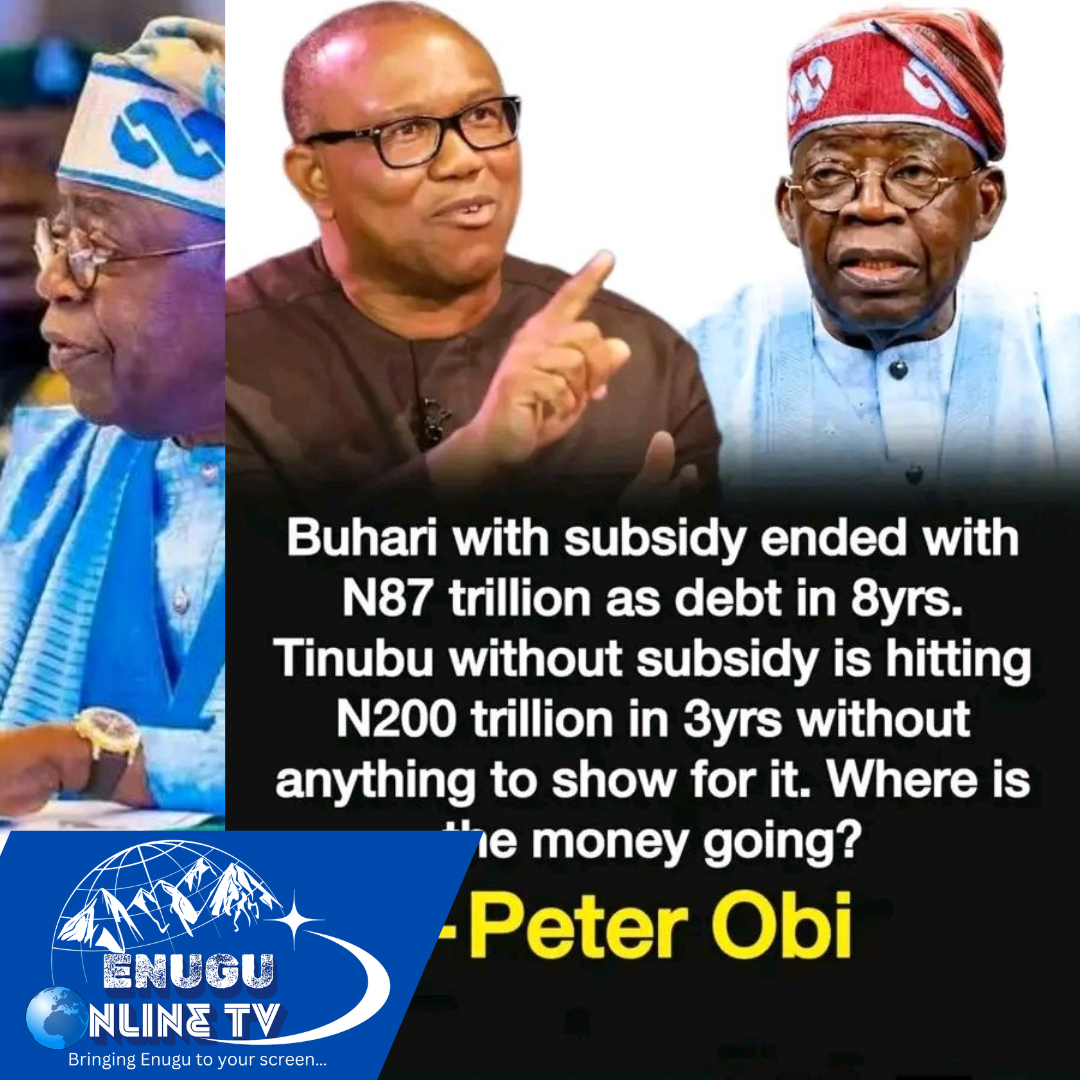

The viral image making rounds online captures a strong comparison between past and present administrations. It highlights that Nigeria reportedly ended the administration of former President Muhammadu Buhari with about ₦87 trillion in debt after eight years, while suggesting that the current administration is approaching ₦200 trillion in just about three years, despite the removal of the fuel subsidy. The statement ends with a critical question: “Where is the money going?”

The claim, rooted in recent public statements made by Peter Obi, is trending widely. Speaking at a political gathering in Abuja, Obi expressed concern that Nigeria’s debt has continued to rise even after the removal of the fuel subsidy, which was originally expected to reduce government spending and borrowing.

According to him, the previous administration left behind a debt figure close to ₦87 trillion, but under the current government, the country’s debt is nearing ₦200 trillion. He argued that the figure represents a significant increase in borrowing despite a major economic reform like subsidy removal, which was supposed to free up funds for development projects.

This development has raised serious questions among Nigerians, especially as many citizens are yet to feel the benefits of subsidy removal. When President Tinubu assumed office in 2023, one of his first major economic decisions was to remove the fuel subsidy, a policy that had long been criticized for draining government resources. While experts, including international financial institutions, had supported the removal as a necessary step, it also led to immediate hardship, including a sharp increase in fuel prices and cost of living.

Now, despite the policy, many Nigerians are questioning whether they are realizing the expected gains as debt reportedly rises. Reactions on social media have been mixed, with some supporting Obi’s concerns and others defending the current administration.

On X (formerly Twitter), some users echoed Obi’s sentiment, arguing that there is little visible development to justify the rising debt. Others pointed to inflation, rising food prices, and unemployment as signs that the economy is under pressure. One user wrote that “if subsidy is gone and borrowing is still high, then something is wrong somewhere,” reflecting a growing sense of frustration among citizens.

However, not everyone agrees with Obi’s position. Supporters of the Tinubu administration argue that economic reforms take time to yield results. They highlight ongoing structural changes, including foreign exchange reforms and attempts to stabilize government revenue. Some also claim that part of the borrowing is necessary to fund long-term infrastructure and stabilize the economy during a difficult transition period.

Debates also arise regarding the accuracy and interpretation of the circulated figures. While data confirms that Nigeria’s debt rose significantly to around ₦87 trillion by 2023, experts often caution that debt figures must be understood within context, including factors like exchange rates, budget deficits, and global economic pressures.

Still, Obi’s statement has succeeded in drawing attention to a key issue of transparency and accountability in government spending. His question, “Where is the money going?” has become a central talking point, with many Nigerians demanding clearer explanations on how borrowed funds are being used.

Beyond politics, this debate reflects the everyday reality of Nigerians. Rising living expenses, currency fluctuations, and economic uncertainty have made people more sensitive to issues of public finance. For many, the discussion is not just about numbers but about how government decisions affect their daily lives.

As the conversation continues to trend, it is clear that Nigerians are paying closer attention to economic policies and their outcomes. Social media has once again proven to be a powerful space for political engagement, where citizens, analysts, and stakeholders can question leadership and demand accountability.

Whether Obi’s claims will lead to further clarifications from the government remains to be seen, but one thing is certain: the issue of Nigeria’s debt profile is now firmly in the spotlight. And as more voices join the conversation, the pressure for transparency and measurable results will only continue to grow.

In the end, the debate is more than just a political statement; it is a reflection of a nation trying to understand its economic reality and demand better for its future.